Journal Entries

A journal entry is a record of the business transactions in the accounting books of business. A properly documented journal entry consists of the correct date, amounts to be debited and credited, a description of the transaction, and a unique reference number.

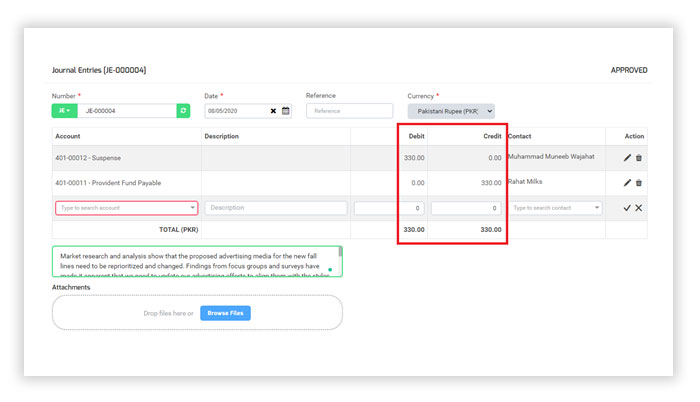

A journal entry is the first step in the accounting cycle. A journal details all financial transactions of a business and makes a note of the accounts that are affected. Since most businesses use a double-entry accounting system, every financial transaction impact at least two accounts, while one account is debited, another account is credited. This means that a journal entry has equal debit and credit amounts.

+Add Journal Entries

- In the left navigation menu select purchase order.

- Click “+Add Journal Entry” to add a new order.

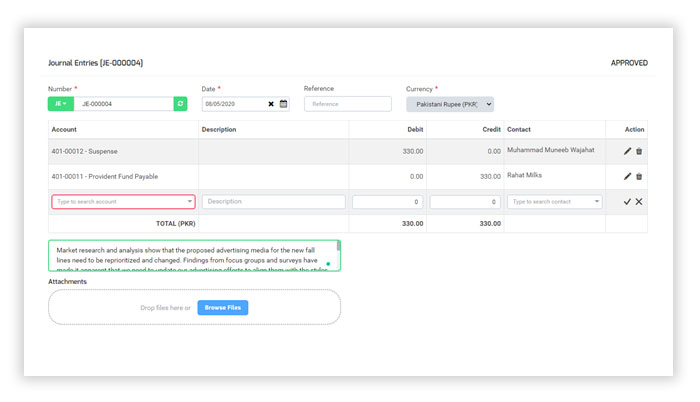

- Numbers: The number will automatically be generated

- Date: This will default to today’s date. You can change this also.

- Click “Save and Continue Edit” to save the quote as a draft, or click “Save and Approve” to approve or click “Save and Pending” to mark the quote as pending and enter a new quote or click “Save and New” to record a new quote and save the previous one or click “Save and Close” to close the quote and save the quote in draft status.

Debit and Credit

Whenever an accounting transaction is created, at least two accounts are always impacted, with a debit entry being recorded against one account and a credit entry being recorded against the other account. There is no upper limit to the number of accounts involved in a transaction – but the minimum is no less than two accounts. The totals of the debits and credits for any transaction must always equal each other so that an accounting transaction is always said to be “in balance.” If a transaction were not in balance, then it would not be possible to create financial statements. Thus, the use of debits and credits in a two-column transaction recording format is the most essential of all controls over accounting accuracy.

Memos for bank Statement

Debit Memo

A debit memo on a company’s bank statement refers to a deduction by the bank from the company’s bank account. In other words, a bank debit memo reduces the bank account balance similar to a check drawn on the bank account

Credit Memo

One type of credit memo is issued by a seller to reduce the amount that a customer owes from a previously issued sales invoice. Another type of credit memo, or credit memorandum, is issued by a bank when it increases a depositor’s checking account for a certain transaction.

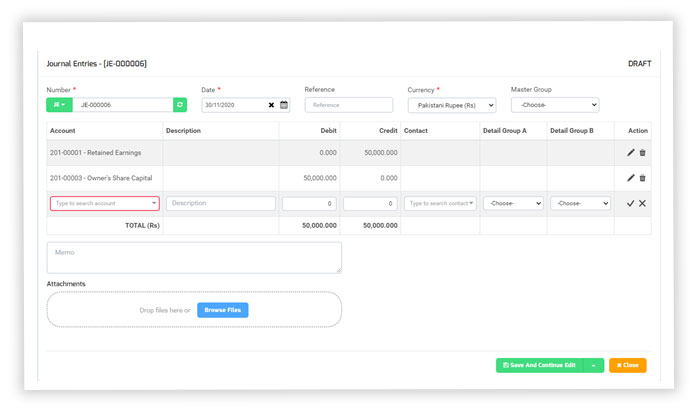

Retained Earnings

Users can now adjust retained earnings directly from journal entries and review respective reports.

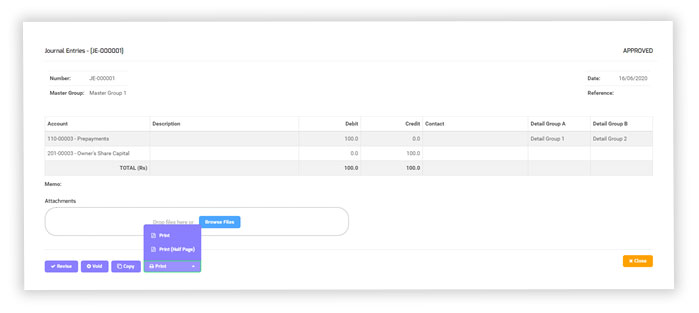

Half page PDF has been added to Journal Entry